OK, so here we are with only a few weeks left to the end of the financial year to get our SMSF in order and ensure we are making the most of the strategies available to us. Here is a checklist of the most important issues that you should address with your advisers before the year-end.

Its been a busy year and I have not had as much time as usual to put this together so if you find an error or have a strategy to add then please let me know. Links were working at the time of writing.

Warning before we begin,

Before we start, just a warning as in the rush to take advantage of new strategies you may have forgotten about how good you have it already Be careful not to allow your accountant, administrator or financial planner to reset any pension that has been grandfathered under the pension deeming rules that came in on Jan 1st 2015 without getting advice on the current and possible future consequences resulting in the pension being subject to current deeming rates if you lose the grandfathering. Point them to this document

- It’s all about timing!

If you are making a contribution the funds must hit the Superfund’s bank account by the close of business on the 30th June. Careful of making contributions through Clearing houses as they often hold on to funds before presenting them to the individual’s superannuation fund for 7-30 days and it’s when the fund receives the payment that the contribution is counted except if paid via the government’s Small Business Clearing House. Pension payments must leave the account by the close of business unless paid by cheque in which case the cheques must be presented within a few days of the EOFY and there must have been sufficient funds in the bank account to support the payment of the cheques on June 30th. Get you payments in by Friday 25th or earlier to be sure (yes I’m Irish).

- Review Your Concessional Contributions options – $25,000 per year up to 67 and $27,500 from 1 July 2021

The government changed the contribution rules from 1 July 2020 to extend the ability to make contributions from age 65 up to age 67. Read more here. Maximise contributions up to concessional contribution cap but do not exceed your Concession Limit. The sting has been taken out of Excess contributions tax but you don’t need additional paperwork to sort out the problem. So check employer contributions on normal pay and bonuses, salary sacrifice and premiums for insurance in super as they may all be included in the limit.

3. If your Super balance on 1 July 2020 was under $500,000 Review your previous Concessional Contributions (CC) and consider using the ‘Carry forward’ concessional contributions cap

Broadly, the carry forward rule allows individuals to make additional CC in a financial year by utilising unused CC cap amounts from up to five previous financial years, providing their total superannuation balance just before the start of that financial year was less than $500,000.

This measure applies from 2018-19 so effectively, this means an individual can already make up to $75,000 of CC (less any Employer or Personal deductible contributons in those years) in a single financial year by utilising unapplied unused CC caps since 1 July 2018 and going forward from up to five previous financial years.

Prior to these amendments, if an individual did not fully utilise their annual CC cap in a financial year, they could not carry forward the unused cap to a later year. But please note the balance refers to $500,000 across all of your Superannuation accounts.

- Review plans for Non-Concessional Contributions (NCC) options

From 1 July 2020 the new age limit of 67 applied to Non-Concessional Contributions (NCC) without meeting the work test so you have the option of making $100,000 NCC per year up to turning 67.

Hopefully this month (tabled for June 2020 sitting) the Senate will also pass the long delayed legislation allowing you to also use the “3 year bring forward rule” up to age 67 this year (currently still not legislated).

So people who turned 64 or 65 this year and who planned to use the “3 year bring forward rule” may want to review that strategy as it will have to be a last minute transfer once the legislation passes. But don’t fret! another solution awaits

From 1 July 2022 the new age limit of 74 will apply to Non-Concessional Contributions (NCC) without meeting the work test so you have the option of making $100,000 NCC per year up to age 74 (specifically turning 75 and 28 Days.)

Current Option if turned 65 in 2020-21 FY: NCC of $100,000 or $300,000

Proposed Option: NCC $100,000 2020-21, NCC $100,000 2021-22, NCC $300,000 2022-23

Opportunities:

- Have you considered making non-concessional contributions to move investments in to super and out of your personal, company or trust name. Maybe you have proceeds from and inheritance or sale of a property sitting in cash.

- Opportunity to even up spouse balances and maximise superannuation in pension phase up to age 74 – Couples where one spouse has exhausted their transfer balance cap and has excess amounts in accumulation are able to withdraw and recontribute to the other spouse who has transfer balance cap space available to commence a retirement phase income stream. This can increase the tax efficiency of the couple’s retirement assets as more of their savings are in the tax-free pension phase environment.

- Make your tax components more tax free by using recontribution strategies – SMSF members can cash out their existing super and re-contribute (subject to their contribution caps) them back in to the fund to help reduce tax payable from any super death benefits left to non-tax dependants. They can now do this until they turn age 75 and 28 days.

- Co-Contribution

Check your eligibility for the co-contribution and if you are eligible take advantage. Note that the limits have changed and it is “free incentive money to save for your retirement” – grab it if you are eligible.

To calculate the super co-contribution you could be eligible to receive based on your income and personal super contributions, use the Super co-contribution calculator.

- Spouse Contribution

If your spouse has assessable income plus reportable fringe benefits and reportable employer super contributions totalling less than $37,000 for the full $540 tax offset and up to $40,000 for a partial offset, then consider making a spouse contribution. Check out the ATO guidance here

From 1 July 2022 you may also be able to implement this strategy up to age 75 as Spouse Contribution treated as a NCC in their account.

Trap: Any spouse contribution is counted towards your spouse’s NCC cap

- Over 67? Do you meet the work test? (The 40 hours in any 30 days rule)

You should review your ability to make contributions as if you if you have reached age 67 you must pass the work test of 40 hours in any 30 day period during the financial year, in order to continue to make concessional contributions to super. Check out ATO superannuation contribution guidance . Again if budget measures pass then from 1 July 2022 you can continue to make salary sacrifice contributions up to age 75 but you will still need to meet the work test to make Personal Deductible contributions.

- Check any payments you may have made on behalf of the fund.

It is important that you check for amounts that may form a superannuation contribution in accordance with TR 2010/1 (ask your advisor), such as expenses paid for on behalf of the fund, debt forgiveness or in-specie contributions, insurance premiums for cover via super paid from outside the fund.

- Notice of intent to claim a deduction for contributions

If you are planning on claiming a tax deduction for personal concessional contributions you must have a valid ‘notice of intent to claim or vary a deduction’ (NAT 71121).

If you intend to start a pension this notice must be made before you commence the pension. Many like to start pension in June and avoid having to take a minimum pension but make sure you have claimed your tax deduction first. The same applies if you plan to take a lump sum withdrawal from your fund. GET THE NOTICE OF INTENT IN FIRST

- Contributions Splitting to your spouse allowed for longer

Consider splitting contributions with your spouse , especially if:

- your family has one main income earner with a substantially higher balance or

• if there is an age difference where you can get funds into pension phase earlier or

• If you can improve your eligibility for concession cards or age pension by retaining funds in superannuation in the younger spouse’s name.

This is a simple no-cost strategy I recommend everyone look at. See my blog about this strategy here.

Trap: Any spouse contribution is counted towards your spouse’s NCC cap

- Off Market Share Transfers (selling shares from your own name to your fund)

If you want to move any personal shareholdings into super you should act early. The contract is only valid once the broker receives a fully valid transfer form not before so timing in June is critical.

- Pension Payments – so many more options this year 2020-2021 and 2021-2022

If you are in pension phase, the government have extended the Temporary Reduction in Minimum Pensions as part of the Covid-19 response. So please ensure you take the new minimum pension of at least 50% of your age-based rate below. For transition to retirement pensions, ensure you have not taken more than 10% of your opening account balance this financial year.

The following table shows the minimum percentage factor (indicative only) for each age group.

Minimum annual payments for super income streams for 2020/21 and 2021/22 Financial years.

| Age at 1 July |

Standard

Minimum % withdrawal |

50% reduced

minimum pension |

| Under 65 |

4% |

2% |

| 65–74 |

5% |

2.5% |

| 75–79 |

6% |

3% |

| 80–84 |

7% |

3.5% |

| 85–89 |

9% |

4.5% |

| 90–94 |

11% |

5.5% |

| 95 or older |

14% |

7% |

FINER DETAILS with TIPS and TRAPS

Here is some of the finer detail on how these measures will work, along with some tips and traps to consider when taking withdrawals for the rest of this financial year and the full 2020-21 financial year:

The measures are forward looking so if a pension member has already taken your minimum pension for the year then they cannot change the payment for this year but they can get organised for 2021/22. So, no you can’t try to sneak a payment back in to the SMSF bank account!

If a pension member has already taken pensions payments of equal to or greater than the 50% reduced minimum amount, they are not required to take any further pension payments before 30 June 2021. For example, many would have taken quarterly or half yearly payments. If they add up to the 50% reduced minimum then you do not need to take anymore payments this financial year.

If you still need your pension payments for living expenses but have already taken the 50% reduced minimum then, it may be a good strategy for amounts above the 50% reduced minimum to be treated as either:

- for those with both pension and accumulation accounts to take the excess as a lump sum from the accumulation account balance to preserve as much in tax exempt pension phase as possible going forward to future years.

- a partial lump commutation sum rather than as a pension payment. This would create a debit against the pension members transfer balance account (TBA). Please discuss this with your accountant and adviser asap as some funds will have to report this quarterly and others on an annual basis. OR

See here for a worked example

- Sacrificial Lamb

Think about having a sacrificial lamb, a second lower value pension that can sacrificed if minimum not taken. In this way if you pay only a small amount less than the minimum you only have to lose the smaller pensions concession rather than the concession on your full balance. When combined with the ATO relief discussed in the following article “What-happens-if-i-don’t-take-the-minimum-pension” you will have a buffer for mistakes.

Before reading the above: Be careful not to reset a pension that has been grandfathered under the new deeming of pension rules that came in on Jan 1st 2015 without getting advice.

- Reversionary Pension is often the preferred option to pass funds to a spouse or dependent child. Review your options

A reversionary pension to you spouse will provide them with up to 12 months to get their financials affairs organised before having to make a final decision on how to manage your death benefit.

You should review your pension documentation and check if you have nominated a reversionary pension. If not, consider your family situation and options to have a reversionary pension.

This is especially important with blended families and children from previous marriages that may contest your current spouse’s rights to your assets. Also consider reversionary pensions for dependent disabled children. T

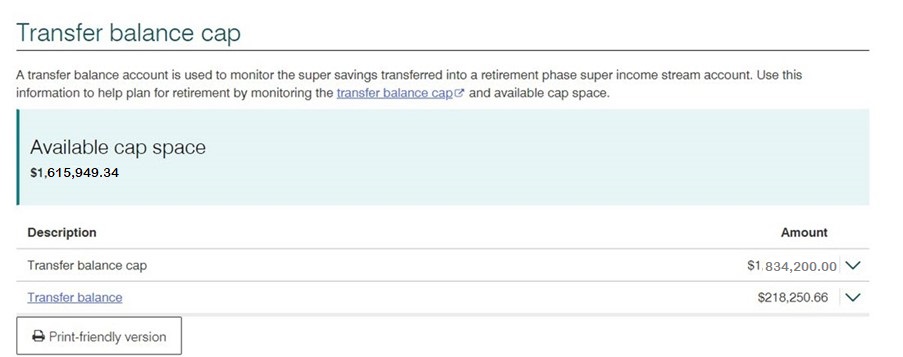

The reversionary pension has become more important with the application of the $1.6m Transfer Balance Cap limit to pension phase.

Tip: If you have opted for a nomination instead then check existing Binding Death Benefit Nominations (many expire after 3 years) and look to upgrade to a Non-Lapsing Binding Death Benefit Nomination. Check you Deed allows for this first

- Review Capital Gains Tax Position of each investment

If you have some funds in accumulation then review any capital gains made during the year and over the term you have held the asset and consider disposing of investments with unrealised losses to offset any gains made in this tax year. If in pension phase then consider triggering some capital gains regularly to avoid building up an unrealised gain that may be at risk to government changes in legislation like those proposed this year.

- Review and Update the Investment Strategy not forgetting to include Insurance of Members

The ATO has now beefed up its requirements for what needs to be detailed in the SMSF Investment Strategy so review your investment strategy and ensure all areas are covered and all investments have been made in accordance with it, and the SMSF trust deed. Also, make sure your investment strategy has been updated to include consideration of insurances for members. See my article of this subject here. You should also visit the ATO’s webpage on the topic here which is very educational Don’t know what to do…..call us.

- Collate and Document records of all asset movements and decisions

Ensure all the funds activities have been appropriately documented with minutes, and that all copies of all statements and schedules are on file for your accountant/administrator and auditor.

- Double Dipping! June Contributions Deductible this year but can be allocated across 2 years.

For those who may have a large taxable income this year (large bonus or property sale) and are expecting a lower taxable next year you should consider a contribution allocation strategy to maximise deductions for the current financial year. This strategy is also known as a “Contributions Reserving” strategy but the ATO are not fans of Reserves so best to avoid that wording! Just call is an Allocated Contributions Holding Account. Note that as the Concessional Limit is moving to $27,500 on 1 July 2021 you can make a total of up to $52,500 using this strategy this year.

- Market Valuations – Now required annually

Regulations now require assets to be valued at market value each year, ensure that you have re-valued assets such as property and collectibles. Here is my article on valuations of SMSF investments in Private Trusts and Private Companies. For more information refer to ATO’s publication Valuation guidelines for SMSFs.

- In-House Assets

If your fund has any investments in in-house assets you must make sure that at all times the market value of these investments is less than 5% of the value of the fund. Do not take this rule lightly as the new SMSF penalty powers will make it easier for the ATO to apply administrative penalties (fines) for smaller misdemeanours ranging from $820 to $10,200 per breach pere trustee.

Covid-Relief – The ATO has responded to current market conditions, and has announced it will not take compliance action against SMSFs where:

- at 30 June 2021 the market value of an SMSF’s in-house assets is over 5% because of the downturn in the share market

- the trustee of the SMSF prepares a rectification plan

- by 30 June 2022, the rectification plan either:

-

-

- cannot be effectively implemented because of market conditions

- does not need to be implemented because the market recovers and the 5% test is again satisfied at 30 June 2022.

For good guidance on this issue https://www.cgw.com.au/publication/what-to-do-if-covid-19-has-ruined-your-smsfs-in-house-asset-ratio-the-atos-no-action-position-for-some-cases/

- Is your fund providing Covid-19 Rent Relief to a property tenant whether a related party or not? Get your documentation in place.

If you have provided Rent Relief to a tenant, related or not, then get it documented now before June 30 that you have considered, managed and documented the request, the reasoning behind the Trustee’s decision and the details of the relief provided

The ATO have thankfully provided a non-binding practical approach of broadly not applying resources to this issue for FY2021. However, this announcement, while positive, should not be relied on given the considerable downside risks.

For detail of what your auditors will most likely require please check Item 3 in this blog https://smsfcoach.com.au/2020/05/22/be-prepared-with-these-9-smsf-audit-tips/

- Careful if replacing TPD Insurance (Total Permanent Disability – basically “never work again” insurance)

Have you reviewed your insurances inside and outside of super? Don’t forget to check your current TPD policies owned by the fund with an own occupation definition as the rules changed a few years ago so be careful about replacing an existing policy as you may not be able to obtain this same cover inside super again.

- Do you need to update to a Corporate Trustee

We recommend a corporate trustee to all clients. To understand why please read this article on Why SMSFs should have a Corporate Trustee

- Check the ownership details of all SMSF Investments

Make sure the assets of the fund are held in the name of the trustees on behalf of the fund and that means all of them. Check carefully any online accounts you may have set up without checking the exact ownership details. You have to ensure all SMSF assets are kept separate from your other assets.

- Review Estate Planning and Loss of Mental Capacity Strategies.

Review any Binding Death Benefit Nominations (BDBN) to ensure they are valid (check the wording matches that required by the Trust Deed) and still in accordance with your wishes. Also ensure you have appropriate Enduring Power of Attorney’s (EPOA) in place allow someone to step in to your place as Trustee in the event of illness, mental incapacity or death. Do you know what your Deed says on the subject? Did you know you cannot leave money to Step-Children via a BDBN if their birth-parent has pre-deceased you?

- Review any SMSF Loans

Have you provided special terms (low or no interest rates , capitalisation of interest etc.) on a related party loan? Then you need to review your loan agreement and get advice to see if you need to amend your loan. Have you made all the payments on your internal or third-party loans, have you looked at options on prepaying interest or fixing the rates while low. Have you made sure all payments in regards to Limited Recourse Borrowing Arrangements (LRBA) for the year were made through the SMSF Trustee? If you bought a property using borrowing, has the Holding Trust been stamped by your state’s Office of State Revenue. Please review my blog on the ATO’s Safe Harbour rules for Related Party Loans here

- Still have Collectibles in your fund?

Play by the new rules that came into place on the 1st of July 2016 or get them out of your SMSF.

- SuperStream obligations must be met

For super funds that receive employer contributions it’s important to take note that since 2014 the ATO has been gradually introducing SuperStream, a system whereby super contributions data is received and made electronically.

All funds should be able to receive contributions electronically and you should obtain an Electronic Service Address (ESA) to receive contribution information. If you are not sure if your fund has an ESA, contact your fund’s administrator, accountant or your bank for assistance.

If you change jobs your new employers may ask SMSF members for their ESA, ABN and bank account details. Some employers may also ask for your Unique Superfund Identifier (USI) – for SMSFs this is the ABN of the fund.

30. ASIC Fees – Increases from 1 July 2021

As expected, ASIC is increasing fees by $1 for the annual review of a special purpose SMSF trustee company $55 > $56. The Government is moving gradually to a “user pays” model so expect increases to accelerate in future years.

For $387 you can pre-pay the company fees for 10 years and lock in current prices with a decent discount. There is a remittance form here:

31.

Reducing the eligibility age for downsizer contributions from 1 July 2022The eligibility age to make downsizer contributions into superannuation will be reduced from 65 to 60 years of age. All other eligibility criteria remain unchanged, allowing individuals to make a one-off, post-tax contribution to their superannuation of up to $300,000 per person from the proceeds of selling their home. These contributions will continue not to count towards non-concessional contribution caps.

The $300,000 downsizer limit (or $600,000 for a couple) and the $330,000 bring forward NCC cap allow up to $630,000 in one year contributions for a single person and $1,260,000 for a couple subject to their contributions caps.

Tip: Great for people who have smaller super balances and invested in their business or property to now switch to tax-effective pensions. You don’t need to have funds available from the sale of your home, that is just the trigger to allow the downsizer contribution and you can use other funds to make the contribution even if you have upsized!.

32. Relaxing residency requirements for SMSFs from 1 July 2022

SMSFs and small APRA funds will have relaxed residency requirements through the extension of the central management and control test safe harbour from two to five years. The active member test will also be removed, allowing members who are temporarily absent to continue to contribute to their SMSF. The Government expects this measure will have effect from 1 July 2022.

Tip: Probably useful post-COVID for those working or travelling to stay with family or get away from them for extended periods overseas.

33 . Legacy retirement product conversions (probably from 1 July 2022)

Individuals will be able to exit a specified range of legacy retirement products, together with any associated reserves over a two-year period. The specified range of legacy retirement products includes market-linked, life expectancy and lifetime products, but not flexi-pension products or a lifetime product in a large APRA-regulated or public sector defined benefit scheme.

Currently, these products can only be converted into another like product and limits apply to the allocation of any associated reserves without counting towards an individual’s contribution cap.

There is considerable additional detail in this feature so consult an adviser if you are affected, especially to ensure you do not lose other entitlements such as the age pension.

This measure will take effect from the first financial year after the date of Royal Assent of the enabling legislation.

34. Improving the Pension Loan Scheme – Social security benefits for you or you mum and/or dad

Current

The Pension Loan Scheme (PLS) allows a fortnightly loan of up to 150% of the maximum rate of Age Pension to help boost a person’s retirement income by unlocking capital in their real estate assets. It can be available for self-funded retirees who are Age Pension age but do not receive a social security pension. Interest is compounded fortnightly at 4.50% p.a., and any debt under the scheme is paid back when the property is sold or the person dies.

Proposal

From 1 July 2022, the Government will introduce a No Negative Equity Guarantee for PLS loans and allow people access to a capped advance lump sum payment.

► No negative equity guarantee

Borrowers under the PLS, or their estate, will not owe more than the market value of their property, in the rare circumstances where their accrued PLS debt exceeds their property value. This brings the PLS in line with private sector reverse mortgages.

► Immediate access to lump sums under the PLS

Eligible people will be able to access up to two lump sum advances in any 12-month period, up to a total value of 50% of the maximum annual rate of Age Pension (currently $12,385 for singles and $18,670 for couples).

Don’t leave it until after 30 June, review your Self Managed Super Fund now and seek advice if in doubt about any matter.

Warning before you jump in to implementation of any strategy,

Before we start, just a warning as in the rush to take advantage of new strategies you may have forgotten about how good you have it already. Be careful not to allow your accountant, administrator or financial planner to reset an account based pension or exit a legacy pension that has been grandfathered under the pension deeming rules that came in on Jan 1st 2015 without getting advice on the current and possible future consequences resulting in the pension being subject to current deeming rates if you lose the grandfathering.

Are you looking for an advisor that will keep you up to date and provide guidance and tips like in this blog? then why now contact me at our Castle Hill or Windsor office in Northwest Sydney to arrange a one on one consultation. Just click the Schedule Now button up on the left to find the appointment options.

Please consider passing on this article to family or friends. Pay it forward!

Liam Shorte B.Bus SSA™ AFP

Financial Planner & SMSF Specialist Advisor™

Tel: 02 98941844, Mobile: 0413 936 299

PO Box 6002 BHBC, Baulkham Hills NSW 2153

5/15 Terminus St. Castle Hill NSW 2154

Corporate Authorised Representative of Viridian Select Pty Ltd ABN 41 621 447 345, AFSL 51572

This information has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on this information, consider its appropriateness, having regard to your objectives, financial situation and needs. This website provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such.

already have a myGovID, you can apply for your director ID now.

already have a myGovID, you can apply for your director ID now.